Supply and demand:

The Heart of the Economy 💖💰

Supply and demand are two fundamental concepts that drive the world economy. They are present in every transaction, from buying a loaf of bread to investing in large technological projects.

But what do they really mean and why are they so important? Let's explore it in a simple way. Here we go! 🚀

What is Supply? 🛒

Supply is basically the amount of goods or services that producers are ready to sell at a specific price.

Imagine you are the genius behind the best lemonade stand in the neighborhood and you decide to sell each glass for $1. If you suddenly raise the price to $2 per glass, you are motivated to squeeze more lemons and make more lemonade to take advantage of the opportunity to earn more 💰.

That is the essence of the law of supply: when the price of a good goes up, the quantity supplied also goes up. It's simple, you want to make more because you are going to earn more! 🤑

Factors that Influence Supply 📊

- Cost of Production: If lemons, sugar, and water become more expensive, you may decide to produce less because it's no longer as profitable. You're not going to want to spend more to earn the same or less, right? 🙄

- Technology: If you get a machine that squeezes lemons at three times the speed, bingo! You can make more glasses of lemonade in less time and with less effort, increasing supply. 🚀

- Weather or External Events: If there's a storm that ruins the lemon harvest, your supply will be affected. Less lemons, less lemonade! 🌧️🍋

What is Demand? 🤝

Demand is the amount of a good or service that consumers want and can buy at a specific price. If the price of your famous glass of lemonade is $1, you might sell 100 glasses a day. But what if you raise the price to $3? People are going to think twice and you might only sell 20.

This is what the law of demand explains: as the price goes up, the quantity demanded goes down. And yes, it works the other way around too. 😉

Factors That Influence Demand 📝

- Price: If you lower the price to 50 cents, get ready for the rush of customers! Everyone is going to want your lemonade. 🏃💨

- Consumer preferences: If your lemonade suddenly goes viral because a celebrity mentions it on social media, get ready for a line of customers. 🤩✨

- Consumer income: If the economy is booming and people have more money, they'll be willing to pay a little more for that refreshing glass of lemonade, and you could raise the price just a little bit. 💵

The Break-Even Point ⚖️

The point where supply and demand intersect is the market equilibrium. Here, the amount of lemonade you produce is equal to the amount your customers want to buy. It's like the “zen point” of the market, where everything is balanced. 🧘♂️

Market Equilibrium Example

Suppose you sell each glass of lemonade for $1 and you can produce 100 glasses. Perfect! Your customers buy exactly those 100 glasses. Now, if you raise the price to $2, some of your customers will say “I'll just go for the tap water,” and you're left with extra glasses. This is excess supply. On the other hand, if you decide to lower the price to 50 cents, you'll have an endless line of customers, but you won't have enough lemonade for everyone, creating excess demand. See how it's all about finding that zen point? 😊

Shifts in Supply and Demand 🔄

In the world of economics, supply and demand are forces that don't stand still. They are constantly changing, influenced by multiple factors that alter how goods and services are produced and consumed. These shifts can change the balance of prices and quantities in the market, generating different effects for producers and consumers. Let's break down how and why these changes happen.

Shifts in Supply 📉📈

Supply, which represents the quantity of goods or services that producers are willing to sell at different prices,

can move on the economic graph due to a variety of reasons:

1. Increased production costs 💸:

If the cost of production of a good rises, for example, if raw materials or energy become more expensive, supply shifts to the left. This means that, at each price level, producers will be willing to offer less of it. A typical example is rising oil prices, which make transportation and production more expensive, reducing the amount of goods that companies can produce at the same cost.

2. Technological Advances 🖥️🔧:

When technology improves, companies can produce more efficiently and at a lower cost. This shifts supply to the right, as producers can offer more at any given price. Think about how automation and improved processes have increased production in factories and assembly plants.

3. Government Policies and Regulations 🏛️:

Taxes, subsidies, and regulations can impact supply. A new tax on a good might shift supply to the left, as it increases the cost of production. Conversely, a subsidy can shift it to the right by reducing costs for producers.

4. Climate Factors and Natural Disasters 🌪️:

The supply of certain products, especially agricultural products, can be affected by weather events. A drought or severe storm can dramatically reduce the amount of a product available, shifting supply to the left.

Shifts in Demand 🔼🔽

Demand reflects how much of a good or service consumers are willing and able to buy at different prices.

Like supply, demand can also change for a number of reasons:

1. Consumer preferences and trends❤️👗

If a good becomes fashionable or is found to have health benefits, demand may shift to the right, indicating that more people want to buy it at any price. For example, if studies show that lemonade is great for your health, demand for lemons and lemonade would increase.

2. Change in consumer income 💰:

If the economy is growing and people have more money, demand for normal goods (like clothing or appliances) shifts to the right. Conversely, in times of recession, when consumer income falls, demand shifts to the left as people prioritize spending on essentials and reduce consumption of additional goods and services.

3. Price of related goods 🔄:

Goods can be substitutes or complements. If the price of a substitute good, such as oranges instead of lemons, rises, demand for lemons might shift to the right as people opt for the cheaper option. On the other hand, if the price of a complementary good, such as sugar, rises, demand for lemons might decrease and shift to the left as making lemonade becomes more expensive.

4. Expectations about the future 🔮:

If consumers expect prices to rise in the future, they might bring forward their purchases, shifting demand to the right. On the other hand, if the price is expected to fall (for example, an upcoming sale or discount), current demand might decrease, shifting to the left.

Impact on Market Equilibrium ⚖️

When supply or demand shifts, market equilibrium also changes. If supply decreases and demand remains constant, the equilibrium price rises and the equilibrium quantity falls. Conversely, if demand increases and supply does not change, prices will also rise, but the quantity supplied will increase.

These shifts can be temporary or persist over the long term, depending on the underlying causes. Understanding them is crucial both for producers, who need to plan production, and for consumers, who must adapt their purchasing decisions.

Impact on the Global Economy 🌍

Supply and demand are the fundamental pillars that move the global economy. Their interaction not only determines the prices of products and services in the market, but also influences aspects such as inflation, economic growth, and the financial stability of countries. Understanding how these forces impact the global economy is key to understanding both the stability and volatility of markets and, ultimately, the daily lives of people around the world.

Global Supply 🏭🚚

Global supply refers to the production capacity and availability of goods and services around the world.This includes everything from natural resources and raw materials to manufactured products and technological services.

- Factors of Production: Supply depends on the availability and cost of factors such as land, labor, and capital. For example, if a country has abundant natural resources and an efficient workforce, it is likely to have a high production capacity and a competitive supply in the international market.

- Supply Chain: Globalization has connected economies into a complex network of supply chains. Any disruptions, such as geopolitical conflicts or natural disasters, can reduce supply and consequently increase prices globally. A recent example is the COVID-19 pandemic, which affected the production and distribution of everything from microchips to food. 🦠🚢

Global Demand 🛒🌐

Global demand is the sum of the desire for consumption of goods and services by individuals, businesses, and governments around the world.

- Economic Growth: When the global economy is expanding, demand tends to increase. Countries with growing economies, such as China and India, have a significant impact on the demand for raw materials and industrial products, driving sectors such as construction and technology. 🏗️📲

- Changes in Consumption: Factors such as per capita income, demographics, and cultural trends influence demand. For example, the rise of the middle class in Asia has increased demand for luxury goods and imported foods.

- Economic Policies: Fiscal and monetary policies of governments and central banks can influence demand. For example, a low interest rate policy can encourage consumption and investment, while high interest rates can reduce demand to control inflation. 💰

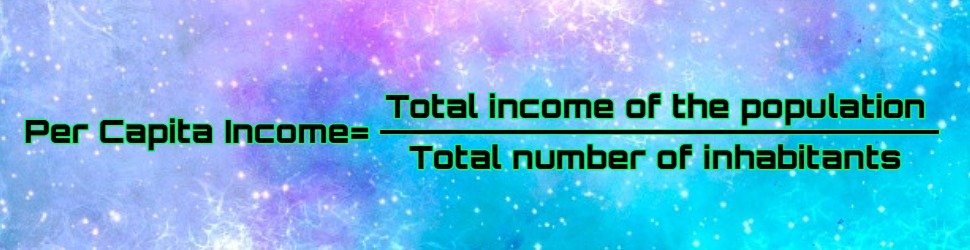

Want to know more? This is Per Capita Income:

Per capita income is an economic measure used to know the average income of a person in a country, region or city in a specific period of time, usually a year. It is calculated by dividing the total income of a population by the number of inhabitants. This measure allows us to get a general idea of the level of wealth or economic well-being of the population of a region, although it does not reflect the inequalities in the distribution of wealth.

Per capita income formula:

Per capita income is used for comparisons between different countries or regions and can help identify the level of economic development or quality of life of a population.

After this pause so you can learn what Per Capita Income is, continue with the article🙏🏻🧑💻

- Economic Policies: Fiscal and monetary policies of governments and central banks can influence demand. For example, a low interest rate policy can encourage consumption and investment, while high interest rates can reduce demand to control inflation. 💰

The Effect of Supply and Demand on Global Prices 💹

The interaction between supply and demand determines the prices of goods and services. When demand outstrips supply, prices tend to rise, causing inflation. On the other hand, an excess of supply in the face of weak demand can lead to deflation, which also has negative effects on the economy.

- Energy and Commodity Prices: Oil prices are a clear example of how global supply and demand impact the economy. If major oil producers, such as OPEC, decide to reduce production, supply decreases and prices rise. This affects transportation and production costs, impacting the final price of products around the world. 🛢️💡

- Impact on Consumers: When prices rise due to high demand or limited supply, consumers tend to reduce their spending. This can lead to an economic slowdown. On the other hand, when prices fall, consumers can spend more, which boosts economic growth. However, a drastic drop in prices can signal deeper economic problems, such as a recession.

Impact on International Trade 🛳️🌎

Variations in supply and demand also affect international trade. If a country produces goods more efficiently and at a lower cost, it will increase its supply and be able to export more, which improves its trade balance. However, if demand in a country increases faster than its production capacity, it is likely to turn to imports, which can affect the trade deficit and the exchange rate of its currency.

The Role of Emerging Economies 📈🌍

Emerging economies play an increasingly important role in global supply and demand. Their rapid growth means an increase in demand for goods and resources, which can put pressure on prices globally. In addition, many emerging economies are large suppliers of raw materials and manufactured goods, which affects global supply.

Conclusion 🔄

Supply and demand are not just abstract economic concepts; they have a tangible impact on the global economy. They determine prices, influence economic policies, and affect international trade. In an increasingly interconnected world, changes in supply and demand in one country can trigger ripple effects felt globally, from the price of bread to interest rates. Understanding these mechanisms is essential to navigating an ever-changing global economic environment. 🌍💡

Key Figures and Related Theories 👥📚

1. Adam Smith 🧔📘:

Considered the father of modern economics, Smith introduced the idea of the "invisible hand" in his work The Wealth of Nations (1776). This metaphor suggests that supply and demand, when functioning freely, lead to economic efficiency without the need for external intervention.

2. Alfred Marshall 📈:

This British economist was the one who popularized the idea of the equilibrium of supply and demand in his book Principles of Economics (1890). Marshall introduced the diagram that we know today, where the supply curve and the demand curve intersect to show the equilibrium point.

3. John Maynard Keynes 📉💡:

Although Keynes is best known for his theories on aggregate demand and government interventions, he also contributed to the understanding of how demand influences the economy as a whole.

Why is it important to understand supply and demand? 🤔

Understanding supply and demand is critical because it influences everyday decisions and economic policy. From business pricing decisions to central bank monetary policies, everything revolves around these economic forces. And as we've seen, knowing how they work gives you a better idea of why prices rise or fall and how your country's economic decisions can affect you.

Impact on Everyday Life 🏠🛒

When you understand supply and demand, common situations make more sense. Ever wonder why the price of gas or milk can suddenly skyrocket? These changes often have to do with supply (production problems, such as droughts) or demand (a surge in global consumption). If consumers know that demand for a product is rapidly increasing, they can prepare to spend more on that good or look for alternatives. 🥛⛽

Also, if you are a business owner, knowing these dynamics helps you set strategic prices, decide when to invest in more inventory, or when to focus on promotions. For example, if you know that a peak sales season is coming up and demand for your products will increase, you can adjust your supply to take advantage of the situation.

Government Policies and Central Banks 🏦📈

Governments and central banks also base their decisions on these forces. A central bank, such as the U.S. Federal Reserve or the European Central Bank, constantly monitors supply and demand to maintain price stability. If demand for products and services outstrips supply, inflation can result. To counter this, central banks typically raise interest rates, which reduces spending and investment, and helps cool the economy. On the other hand, if supply is plentiful and demand is low, there could be deflation, which is also problematic. In these cases, banks may lower interest rates to stimulate the economy. 🔄💰

Supply and Demand in International Markets 🌐💹

Globalization has made supply and demand impact far beyond the borders of a single country. For example, if China experiences an increase in demand for raw materials, prices in other parts of the world may also rise. This affects the global economy and can influence the economic policy of several nations at the same time.

Trade agreements, tariffs, and import/export policies are tools that governments use to balance supply and demand between countries. A change in import tariffs, for example, can alter the supply of products in a country and change prices for consumers.

Application in Financial Education 💡📚

Knowing how supply and demand work is also a key skill for financial education. It allows people to better understand market trends, assess when it is a good time to buy or invest, and prepare for periods of inflation or deflation.

In investing, stock and real estate prices often move due to changes in supply and demand, and informed investors use this knowledge to make smarter decisions. 📈🏠

A World in Motion 🌍🌀

The world is an interconnected place where events in one country can influence global supply and demand. From a geopolitical crisis affecting oil supply to a technological advancement increasing the supply of digital goods, these forces not only influence markets, but also shape the world we live in.

conclusion🎯

Understanding how supply and demand influence the global economy gives you an edge in anticipating economic changes and making more informed financial and consumer decisions. It's not just about understanding why products go up in price at the grocery store, but understanding how every part of the economic system is interconnected and how small variations can have a ripple effect across the globe. 🌍📊

I hope that after reading this article, the next time you buy something or watch the economic news, you understand a little better the “why” of prices and the balance that moves the world. 🌎🛒💸. Ready to see the economy with different eyes?

Now that you know what Supply and Demand are, delve deeper into each section, from Mesopotamia to the present day. Learn how it all began ⬇️𓀌➡️🏛️➡️🕌➡️🏰➡️🏢⬇️

🏁Let's start the journey on economics and finance from the cradle of civilization to the present day. Learn with $WAFFT

Mesopotamia: The World's First Economic Revolution

Development of barter trade and the first accounting records on clay tablets🌾💼

Ancient Mesopotamia, known as "the land between two rivers" (the Tigris and Euphrates), was the scene of some of humanity's first great advances, including the creation of writing, the establishment of the first cities, and of course, the development of a complex trade network that linked different cultures and regions of the ancient world. If you want to know how trade worked in one of the first civilizations in history, join me on this journey into the past! 🚀📜

The Geographic Context and its Influence on Trade 🌍

The geography of Mesopotamia played a crucial role in the development of its economy. Located in what is now Iraq and parts of Syria and Turkey, this region was a fertile plain that depended on the Tigris and Euphrates rivers for agriculture. However, despite being rich in agricultural resources, the area lacked essential raw materials such as metals and wood. This need drove trade with neighboring regions that could provide these materials. 🗺️

From Villages to Cities: The Rise of Organized Trade 🏙️

During the Ubaid period (approximately 6500-3800 BC), agricultural villages began to grow and develop into urban centers. These centers, such as Uruk, Eridu, and Ur, became the first epicenters of organized trade. Barter, which was initially limited to local exchanges, began to evolve into more complex transactions involving distant communities.

With the arrival of the Early Dynastic period (2900-2334 BC), the expansion of city-states led to an increase in demand for goods and resources. Trade became more organized and regulated, with temples and palaces playing a fundamental role in the economy. These institutions not only controlled large tracts of land, but also the production and distribution of goods. 🏛️

The Rise of Uruk and Large-Scale Trade 🌆

One of humanity's first great cities, Uruk became a true economic and cultural center during the Uruk period (approximately 4000-3100 BC). Trade routes were established here, connecting Mesopotamia with Anatolia, the Levant, and the Indus Valley. The invention of the wheel and the sail during this period facilitated the transport of goods, both by land and water, revolutionizing long-distance trade. 🚚⛵

Trade Routes: Connecting the Ancient World 🛣️

Mesopotamian trade was not limited to the local region; it extended over vast distances. Merchants traveled along land and river routes that connected Mesopotamia with Anatolia (present-day Turkey), the Levant (present-day Syria, Lebanon, and Israel), Iran, and as far as the Indus Valley (present-day Pakistan and northwest India). Through these routes, the Mesopotamians exchanged products such as:

Copper and tin: necessary for the manufacture of bronze, they came mainly from Anatolia and Iran.

Wood: scarce in Mesopotamia, it came from the mountains of Anatolia and Lebanon.

Precious and semi-precious stones: such as lapis lazuli, which arrived from the mines of Badakhshan, in Afghanistan.

Textiles and food: produced in Mesopotamia itself and exported to neighboring regions.

These exchanges were not only carried out by land, but also through waterways and the Persian Gulf, facilitating the connection with the cultures of the Arabian Peninsula and beyond. 🌊

Sargon of Akkad: Unification and Expansion of Trade 🌍

One of the most important figures in the history of Mesopotamian trade was Sargon of Akkad (2334-2279 BC). Sargon founded the first known empire in history, the Akkadian Empire, unifying much of Mesopotamia under his rule. This unification process facilitated trade by reducing conflicts between city-states and establishing safe trade routes. In addition, Sargon is known to have organized trade expeditions to distant lands, such as the Indus Valley and the Dilmun region (present-day Bahrain), in search of precious metals and other raw materials. 🌐

Cuneiform Writing: The World's First Accounting! 📜✍️

The growth of trade brought with it the need to keep accurate records of transactions. It was then that one of humanity's greatest innovations emerged: cuneiform writing, developed around 3200 BC in the city of Uruk. This form of writing was used to record contracts, inventories, and trade agreements on clay tablets. 🏺

Merchants and scribes recorded everything: from the amount of grain exchanged for heads of cattle, to the interest on a loan. Yes, they had loans and credits too! This system not only facilitated trade, but also laid the groundwork for modern accounting.

The Ur III Period: The Golden Age of Mesopotamian Trade 💰

The Ur III Dynasty (2112-2004 BC) marked a period of great commercial prosperity and economic expansion. During the reign of Shulgi (2094-2047 BC), paved roads were built and relay stations were established along trade routes, facilitating the transit of merchants and goods. Shulgi also implemented a system of standardized weights and measures and promoted the use of the shekel, a measure of weight used for trade, similar to an early currency.

During this time, Ur became the most important commercial center in Mesopotamia, where goods were traded from as far away as the Arabian Peninsula, the Persian Gulf region, Elam (southwestern Iran), and the Indus Valley. Ur III's administration also encouraged internal trade, establishing regulated markets in key cities. 🏛️

The First Banks and Credit: The “Financiers” of Mesopotamia 💰🏦

In ancient Mesopotamia, temples and palaces were not only religious and political centers, but economic ones as well. They acted as the first banks, where merchants and citizens could deposit their goods, obtain loans, and make investments. These loans, usually in the form of goods such as grain or livestock, had to be repaid with interest, which was usually set at 20%.

A notable figure in this field was Dudu of Uruk, who served as a banker during the reign of Ur-Nammu (2112-2095 BC) and provided credit for commercial expansion. This system not only benefited merchants, but also farmers, who used the loans to finance their crops. If the crop failed, they could restructure the loan, although harsh conditions were often imposed. As a result, many people ended up in debt and lost their land, a problem that led to the enactment of debt forgiveness laws in some periods of Mesopotamian history. 📉

International Trade and Diplomacy: Exchange of Ideas and Goods! 🌏🤝

Mesopotamian trade was not limited to the simple transaction of goods. Trade exchanges were also a means for the spread of ideas, technologies, and customs. Through contact with other cultures, Mesopotamians learned and adopted new agricultural techniques, writing systems, and administrative models.

Trade agreements were often linked to diplomatic treaties. For example, King Hammurabi of Babylon (1792-1750 BC), known for his famous code of laws, also promoted trade treaties with neighboring kingdoms. These agreements facilitated access to valuable resources such as tin and copper, essential for the production of bronze, as well as timber from Lebanon. These diplomatic and trade relations were vital to the stability and prosperity of the region. 🗿

Merchants and Their Adventures: The Adventures and Challenges of Early Entrepreneurs 🧳🚚

Mesopotamian merchants were true adventurers. They often traveled long distances, facing dangers such as raiders, extreme weather conditions, and the threat of war. But they were not alone on these journeys; they often traveled in well-organized caravans with guards to protect their goods.

To facilitate trade, rest stops known as “karums” were established along trade routes, especially in Anatolia. These centres functioned as warehouses, markets and resting places, and were managed by merchant associations that ensured fair trade and mutual protection. The most famous karum was located in the city of Kanesh (present-day Kültepe, Turkey) and was an important trading centre during the Early Assyrian period (ca. 1900-1750 BC). 🏕️

The Laws of Trade: Hammurabi's Code and Transaction Rules ⚖️

Trade in Mesopotamia was not a "wild west"; there were strict laws regulating transactions. The Code of Hammurabi (ca. 1754 BC), one of the oldest known sets of laws, included specific rules for trade, such as tariffs for the transport of goods and regulations for loans and interest.

For example, the code stated that if a merchant borrowed money for a trading voyage and the ship sank, the debt was cancelled. However, if the merchant survived, he was required to pay back the loan with interest. Severe penalties were also stipulated for fraud and breach of contract, which helped maintain confidence in the system.

The Fall of Babylon and the Transformation of Trade 🚪

The fall of the Babylonian Empire to the Persian Empire in 539 BC marked the end of an era in the history of Mesopotamian trade. However, under Persian rule, trade continued to flourish. The Persians built a vast network of roads, known as the Royal Road, which connected Susa (in Elam) to Sardis (in Anatolia). This network further facilitated trade and communication between the different regions of the empire. 🛤️

Conclusion: Mesopotamia, the Cradle of Modern Trade 🌟

Trade in ancient Mesopotamia was not only an economic driver, but also a key factor in the cultural and technological development of humanity. From humble beginnings of bartering in small villages, to the creation of international trade routes and primitive banking systems, the commercial history of Mesopotamia is one of innovation and adaptation.

Thanks to their ingenuity and entrepreneurial spirit, the Mesopotamians laid the groundwork for many of the economic practices we use today. So the next time you go shopping or negotiate a contract, remember that you are following in the footsteps of these pioneers of trade. The legacy of Mesopotamia lives on in every transaction we make! 💼🛒

Egypt: Welcome to the fascinating world of trade in the ancient world! 🌍📜Coin creation and maritime trade

Egypt wasn't just the land of pharaohs, pyramids, and hidden mysteries; it was also a super-important trading center of antiquity. From bartering with nearby neighbors to expeditions to faraway lands, the Egyptians knew how to keep the economy going, even when something as simple as money didn't exist. So, pack your explorer's backpacks and let's travel together through the markets and trade routes of ancient Egypt. 🚶♂️💼

1. Why was trade so important? 🤔

Imagine you're at home and need to buy food, clothes, or any basic things. If you live in a modern city, you take a walk to the supermarket or shop online and you're done. But in ancient times, things weren't that simple. Although Egypt was a super-rich country in resources, like grain, papyrus, and gold, there were things it simply didn't have. To get those missing products, the answer was trade.

Since very ancient times, in the Predynastic Period (we're talking about 6000 BC!), the Egyptians were already exchanging goods with each other. 🏺🛶 But they didn't stop there. As their civilization grew, so did their interest in what lay beyond their borders.

2. How did the economy work without money? 💸❌

This is where things get interesting. Before the Persians arrived and brought the concept of coins (in 525 BC), the Egyptian economy was run on a barter system. Barter? Yes, that “I'll trade you this for that” thing. But don't think it was a random exchange, they had their own “standard of value” called deben! 🏋️♂️

The deben was not a physical coin, but a measure of value that was equivalent to about 90 grams of copper. So if you wanted a scroll of papyrus and it was worth one deben, you could trade it for something that was also worth the same amount, like a pair of sandals or three mugs of beer. Papyrus wasn't cheap! 📜🥖👡

In addition to copper, there were also gold or silver deben for the more expensive things. So basically, Egyptians could buy and sell without needing coins, using a system that everyone understood and accepted. 📈🤓

3. From the corner store to international trade 🌐

The Egyptians started with local trade between Upper and Lower Egypt, exchanging goods according to region. But when the kings of the First Dynasty (3150 BC) consolidated power, they began to look beyond their borders. This is how they came to trade with Mesopotamia, Nubia, and the Levant. Egypt was no longer a small player, it was now in the international league! 😎⚽

In Nubia, which was to the south, they found gold mines. They liked it so much that the name Nubia itself comes from the Egyptian word “nub”, which means gold. And since sometimes diplomacy was not enough, they decided to go and “negotiate” with armies. King Djer of the First Dynasty did not beat around the bush and secured several trading centres in Nubia with the stroke of a sword. 🗡️💰

4. Routes and means of transport: In adventure mode! 🗺️🦓

To move their goods, the Egyptians did not limit themselves to using donkeys and papyrus boats. As trade expanded, their means of transport evolved as well. They traded fragile papyrus boats for sturdier wooden ships capable of sailing long distances.

One of their favorite destinations was Lebanon, from where they brought back the precious cedar wood to build everything from temples to sarcophagi.🚢🌲

There were also land routes through the desert. One of the most important was the Wadi Hammamat, which connected the Nile to the Red Sea. Goods were tied on the backs of donkeys, and caravans were accompanied by armed escorts to prevent bandits from stealing the “souvenirs.” 🏜️🐪🔫

5. The Jewel in the Crown: Yam 💎🐘

One of the most important trading centers in Nubia was called Yam, mentioned in Egyptian texts as a source of wood, ivory, and of course, more gold. Although its exact location is a mystery (Indiana Jones, where are you when we need you?!), it is believed to have been in the Shendi region of modern-day Sudan. Yam was a vital trading center during the Middle Kingdom (2040-1782 BC) before disappearing from the map and being replaced by another place called Irem. 🗺️🦛

During the New Kingdom (1570-1069 BC), Egypt was at its peak and trading with more countries than ever before. Hatshepsut, the most famous pharaoh, organized the famous expedition to Punt (present-day Somalia), from where she brought back ships full of frankincense, myrrh, and trees. Yes, whole trees! 🛳️🌳

6. It wasn't all gold! Other products that flew in the market 🛒

Although gold was the most sought after, Egypt traded a lot of other products. They had so much grain that in Roman times they became “the granary of Rome.” In addition, they exported linen, papyrus, leather goods, and pottery. In return, they received wood, metals, and precious stones that they didn't have at home. 🏺📜

Interestingly, the papyrus they exported to Byblos (in the Levant) was so famous that the word “Bible” comes from it. That’s how influential Egyptian trade was! 🏛️📖

7. Trade and culture: More than just transactions 💬🌍

Trade not only moved products, but also ideas, beliefs, and technologies. The Egyptians borrowed many things from their neighbors, such as the use of cylinder seals from Mesopotamia or artistic designs. Cultural exchanges through trade created a melting pot of cultures in the ancient Mediterranean. 🏺🎭

The Greek city of Naucratis, in the Nile Delta, became an important commercial and cultural center, and Alexandria would later take over as one of the most important cities in the ancient world. Egypt traded with Cyprus, Crete, Greece and Syria, receiving products as diverse as wine, oil, resin, and livestock in exchange for its own treasures. 🍇🥖

8. Beware of thieves! 🏴☠️

Trade was not always a bed of roses. Sometimes caravans were attacked by bandits, and merchants had to be prepared to defend themselves. During the New Kingdom, Egypt established a police force to protect trade routes, collect tolls, and ensure that merchants arrived safely.

Wenamun, an Egyptian merchant who was sent to buy wood for Amun's ship, experienced the danger of trade firsthand: he was robbed at the port and didn't get much help from the local governor. So he decided to steal from someone else! 😅

9. Trade as the engine of civilization 🔄🏛️

Trade was essential to finance many of Egypt's great works, such as the pyramids of Giza, the Temple of Karnak, and the mortuary temple of Hatshepsut. But it wasn't just about building monuments; trade kept society in balance. By sending products to the temples and the people, the king showed that he was looking after his subjects and respecting the principle of ma'at (harmony). If the economy was doing well, it meant that the pharaoh had the favor of the gods. 🌞👑

10. The legacy of Egyptian trade 🏺📜

Trade in ancient Egypt not only enriched the pharaohs, but connected cultures and created a network of exchange that reached to the heart of the Mediterranean. Even as times changed, the Egyptians continued to trade for millennia, adapting to new challenges and opportunities. Their trading legacy lives on in the history of global trade and reminds us that there will always be something to learn and share beyond our borders. 📚🌍

So, the next time you buy something in a store or trade cards, think of the ancient Egyptians, who were already trading and connecting the world long before Amazon existed. 🚀📦 Thanks to them, trade is, and always will be, the engine that drives the world!

Trade in Ancient Greece: the engine of the economy 🏛️

From very ancient times, the Greeks were already looking for ways to exchange products and get hold of things that they could not produce on their own lands. Remember that the geography of Greece is a bit complicated: mountains everywhere and many islands scattered around. This made some regions very good for certain things (like olives and wine in Athens) and others not so much (the lack of good wheat fields, for example). 🌾🫒

So, from very early on, trade was not an option, it was a necessity! But, be careful, things were not always the same. For example, in the Bronze Age (around 2000-1100 BC), civilizations like the Minoans in Crete and the Mycenaeans in mainland Greece already had trade networks throughout the Mediterranean. 🏺🇬🇷 Objects from these cultures were found as far away as Egypt and Asia Minor! Amazing!

However, everything went down the drain around 1100 BC, with the arrival of the famous "Dark Ages" (nothing to do with "Game of Thrones" 😅). For a few centuries, trade practically disappeared, and the Greeks were somewhat isolated. Who saved the day at this time? The Phoenicians! These trade geniuses kept the routes active and continued to exchange products throughout the Mediterranean.

Rise of Greek trade! 🚀

Around the 8th century BC, the Greeks got their act together again. 🎉 The texts of Homer and Hesiod already mention markets (emporia) and merchants (emporoi), although, of course, the Greek elite still thought that engaging in trade was "undignified" for them. But who cared? Trade was booming! ⛵

From 750 BC, international trade exploded. Why? Well, here's where things get interesting:

Greek colonization: The Greeks weren't content to stay at home. They founded colonies in southern Italy (Magna Graecia), on the Black Sea coast, in North Africa... everywhere! These colonies became key points for trade. 🏛️

Currency and measurements: Coins began to be used regularly, which made trade much easier. Bartering was no longer necessary! Measurements were also standardized, which prevented confusion and scams. 🪙⚖️

New routes and technologies: The construction of specialized trading ships and the creation of the famous diolkos (a path through the Isthmus of Corinth) made it easier to transport goods throughout the Mediterranean. 🌊

Security at sea: Goodbye pirates! 🏴☠️ Well, not entirely, but security on trade routes improved quite a bit. This made it safer for merchants to take their goods to faraway places.

What was traded in Greek trade?

Now, let's get to the interesting part: what products were all the rage in Greek markets? Spoiler alert! Wine and olives were the stars of the show! 🍷🫒 But there was so much more.

Greek Exports (What the Greeks Sold!) 📤

Wine: Greek wine, especially from islands like Mende and Kos, was famous all around the Mediterranean. It was transported in large amphorae and sold almost everywhere. 🍇🍷

Olive Oil: Just as famous as wine, Greek olive oil was used for cooking, as a cosmetic, and even in religious rituals. 🫒

Pottery: The Greeks were experts at making decorated vases and amphorae, especially in places like Athens and Corinth. Their pottery was highly prized and has been found as far away as the Atlantic coast of Africa! 🏺

Bronze and Marble: Bronze and marble artifacts were other popular products that the Greeks exported. Marble from Naxos and Athens was particularly valued. ⚒️

Greek Imports (What the Greeks Bought!) 📥

Grain: Being a scarce resource in Greece, grain was imported in large quantities, especially from the Black Sea and Egypt. 🌾

Slaves: Slaves came from all over the Mediterranean, but especially from Egypt and the Black Sea. 👤

Salted Fish: Coming from the Black Sea, it was one of the most consumed products. 🐟

Wood: A lot of wood was needed, especially for shipbuilding. The best wood came from Macedonia and Thrace. 🌲

Precious metals: Gold, silver, copper, iron... everything was imported for the manufacture of tools, weapons and ornaments. ⚒️💰

How did they protect trade? 🤔

Trade in ancient Greece was risky! 🌊 Ships could sink, be attacked by pirates, or not reach their destination due to storms. To mitigate these risks, the Greeks invented maritime loans. How did they work? Simple: if the ship arrived safely, the merchant would repay the loan with interest (which could be between 12.5% and 30%). But if the ship didn't arrive, the merchant didn't have to pay anything back! 😱 A kind of insurance, but with high interest.

In addition, the Greeks took measures to ensure that certain products, such as grain, were always available. In Athens, grain was so important that there was an official “grain buyer” called a siton, and re-exportation of this product was prohibited under penalty of death. 😬

Taxes and Regulations 💰

Despite being a civilization based on trade, the Greeks did not pass up an opportunity to tax. In cities like Athens, there were taxes for foreign merchants who wanted to sell their products in ports. There was even a special tax for ships crossing the Bosphorus – and they weren’t in Athens! 😅 In addition, private banks facilitated currency exchanges and money storage, which made the economy more sophisticated.

Athens, the king of trade in the Mediterranean 🏛️

If there was one place that dominated trade in the Mediterranean during the 5th century BC, it was Athens. With its famous port at Piraeus, Athens became the place where everyone wanted to trade. The Athenians offered tax advantages, security, and an efficient judicial system to attract traders. It was like the commercial hub of antiquity! 😎

What happened next? 😢

The decline of the Greek city-states, especially after the Peloponnesian Wars and the expansion of the Macedonians, caused trade to move to other regions. However, Greek cities, such as Athens and the free ports of Delos and Rhodes, remained important trading centers during the Hellenistic and Roman eras. 🏛️

In summary...

Trade in ancient Greece was much more than just an economic activity; it was the central axis of their civilization. Through the exchange of goods, the Greeks not only got what they needed, but also spread their culture, art, and ideas throughout the Mediterranean. 🌊 So the next time you think of ancient Greece, remember that their power came not only from their army or their philosophers, but also from their merchants and their sea routes! 💡

Persian Empire: The first centralized tax system 💰🏛️🕌

Have you ever wondered how the economy of one of the largest empires in history worked?🕌

The Persian Empire had it all under control! It was one of the first to develop a centralized tax system, and not only that, but it also mastered trade, agriculture, and finance on a grand scale. So buckle up because we're going to travel back a few centuries and find out how ancient Persia managed its wealth and maintained its gigantic empire.

The Rise of Persia: The Economic Machine Begins 🕌🔧

The Persian (or Achaemenid) Empire, founded by Cyrus the Great in 550 BC, was a behemoth that spanned three continents: Asia, Europe, and Africa. To hold such a vast and diverse territory together, they needed more than just good intentions. Persia designed an economic system so advanced that it became the benchmark for future empires.

Cyrus was not only a military genius, but also an economic strategist. His goal was to maintain stability in conquered regions and encourage economic growth through a fair tax system and efficient administration. And boy did he succeed!

The First Centralized Tax System 💰🧾

Before the Persians came, many empires had tax systems, but they were rather chaotic. Each region did things its own way, making it difficult to maintain real control over revenue. Darius I, who ruled from 522 to 486 BC, changed all that. It was he who put in place a centralized tax system that became the backbone of the Persian economy.

And how did it work? 🤔

Satrapies: Persia was divided into provinces called satrapies, each under the command of a governor or "satrap." These regions paid tribute to the emperor based on their wealth. It was not a one-size-fits-all system, but each region paid according to its means. 💸

Fair Taxation: Darius was aware that if he squeezed his subjects too much, the empire could collapse. So each satrapy contributed according to its economic capacity. For example, the wealthy regions of Babylon paid more in taxes than the mountainous and less productive regions of the east. 🏞️

Accurate Accounting: The empire had royal inspectors who watched over the satraps to make sure they weren't embezzling funds or being corrupt. Kind of like auditors from ancient times! 🧐

Standardized Currency: Before Persia, each region used its own currency, which made trade difficult. Darius introduced the empire's first standardized currency: the daric, made of gold, and the silver shekel. These coins not only facilitated internal trade, but became a symbol of imperial authority. 💰

The Backbone of the Economy: Agriculture and Trade 🚜🛤️

Once a solid tax system was established, the Persian Empire set about developing its most important sectors: agriculture and trade.

Agriculture: The Kings of Irrigation 💧🌾

Although much of the empire was in arid or semi-arid regions, the Persians were not intimidated by geography. They invented qanats! 😮 These were underground tunnels that carried water from aquifers to agricultural areas, ensuring a constant supply of water even in the driest times. Cool, right? 💦🌱

They grew wheat, barley, vines (to produce wine), and fruits such as dates, pomegranates, and figs. All of this not only fed the population, but also generated a surplus that could be traded both within and outside the empire.

Trade: A Global Crossroads! 🌍🚢

Persia was at the center of the main trade routes of antiquity. The Silk Roads crisscrossed the empire, bringing silks, spices, and other riches from Asia, while the Persians exported goods such as gold, silver, carpets, perfumes, and agricultural products. 🏺👗

In addition, the Persians had an impressive road system, such as the Royal Road that connected Susa (in the heart of Persia) to Sardis (in Asia Minor). This road not only facilitated trade, but also the administration of the empire, as it allowed the rapid movement of soldiers and messengers. They were like the highways of antiquity! 🛣️

Key figures in the Persian economy 🕌💼

Cyrus the Great (559-530 BC):

Founder of the empire. Although best known for his military skill and religious tolerance, he was also an economic innovator. Cyrus understood that to rule a diverse empire, he needed an economic system that allowed all cultures to thrive.

Darius I (522-486 BC):

The real brains behind the centralized tax system. He not only organized tax collection, but also built the infrastructures that kept Persia at the forefront economically for centuries. Darius was the king who turned Persia into a “functioning empire.” 💼

Xerxes I (486-465 BC):

Although best known for his clashes with the Greeks (the famous Battle of Thermopylae!), Xerxes continued Darius’ economic policies and kept wealth flowing through the empire.

Persian Coinage: Symbol of Power 🪙💪

The gold daric and silver shekel were not only means of exchanging goods, but were also symbols of imperial power. They had engravings of the king, reminding everyone who was in charge. With these coins, Persia was able to facilitate trade both within the empire and with other states, such as the Greeks or the Phoenicians.

Before the introduction of the daric, Persians exchanged goods through barter or used foreign currencies, but Darius sorted out this chaos. The daric became the go-to currency throughout the ancient world. 💰🌏

Innovations in Banking and Insurance 🏦

The Persians also pioneered the concept of banking and insurance. To protect merchants and caravans traveling long distances, the Persians developed a system of commercial loans and insurance that covered losses from theft or natural disasters. If a caravan lost its cargo along the way, the merchant did not lose everything. This system was essential to fostering trade and ensuring economic stability.

International Trade: The World Was Their Market 🌍🚀

International trade was key to Persia's wealth. The Persians traded with Egypt, India, China, Greece, and the Mediterranean. Persia was the connection point between East and West. They imported silk, spices, precious stones, and porcelain, while exporting carpets, perfumes, precious metals, and agricultural products. 🌾💎

During Darius' reign, trade with Greece and the Mediterranean flourished, creating a constant exchange of goods, ideas, and technologies. In fact, Persian economic influence was so great that it even affected the currency and culture of other civilizations.

Conclusion: An Empire Built on Economics 📈🕌

The economy of the Persian Empire was a marvel of antiquity. With its centralized tax system, innovative infrastructure, and ability to manage large-scale international trade, Persia became an economic superpower. Its legacy has influenced global economic history for centuries. So the next time you think of great empires, remember that it wasn't all battle and conquest. There was also an economic machine working behind it all, and Persia was a master of this art! 🌍🚀

So far the first part of the economic guide since the beginning of civilization, let's go with part 2

(500 b.C. - 476 a.C.)

Economy of the Roman Empire:

the foundations of the primitive banking system 🏛️💵

Let's travel back in time to the great Roman Empire! 🏛️ A colossus not only in the military and cultural, but also in the economic. In this article I will tell you how the Romans developed a primitive banking system, how they established laws for trade and property, and how Roman coins facilitated trade throughout the Mediterranean and beyond. All this in a simple, direct tone and with many details that will make this trip a memorable experience. Here we go!

1. The development of the primitive banking system: The first bankers of Rome! 🏦💰

The banking system in Rome started very simply, but became essential to its economy as the empire expanded. During the first centuries of Rome, back in the 4th century BC, the Romans barely used banks as we know them today. However, as the city became an economic center, the first private bankers, known as argentarii, emerged. These bankers operated in markets and tabernae (trading establishments), helping people store their money, lend, and exchange currencies from different regions. 💵

To give you an idea, the argentarii were a kind of “money exchange.” As the Roman Empire grew across the Mediterranean, there were a lot of different currencies in circulation, creating a need for currency exchange services. If a merchant from Greece wanted to buy oil in Hispania, or if a Roman soldier was getting paid on a campaign in Britain, the bankers were the ones who made sure the right money was available.

In addition, the bankers offered loans. Imagine you are a merchant in Pompeii and you need to buy goods to take to Carthage; the argentarii would lend you the money, but with interest, of course (around 12%, although rates could vary). These loans were key to the economy, as they allowed merchants to operate on a large scale. 📈💸

However, the system was not perfect. Since there were no central institutions like today, trust in bankers depended heavily on personal reputation. If a banker committed fraud or was unable to pay his clients, the situation could become very complicated. But, like every good Roman, the money always found its way! 👀

2. Laws to regulate trade and property: Rome and the legal order! 📜⚖️

If there was one thing that characterized the Roman Empire, it was its obsession with laws. For the Romans, laws were not only essential to maintaining social order, but also to regulating trade and property. And no wonder, when your empire spans from Hispania to Egypt, it is essential to have a common legal framework to ensure that business transactions are carried out smoothly.

One of the earliest sets of Roman laws was the Law of the Twelve Tables (Lex Duodecim Tabularum), which came about in the 5th century BC. These laws, while not specifically focused on trade, laid the groundwork for property rights and contractual disputes. If you bought a house or land in the countryside, there were clear laws protecting your right to ownership. And, if any conflict arose (which was fairly common), the legal system ensured that it could be resolved fairly. 🏘️🏞️

But beyond property laws, the Romans developed a very advanced legal system to regulate international trade. As the empire grew, Roman merchants encountered different legal systems in each region. To simplify things, the Romans created what they called "Ius Gentium," a sort of common law that governed transactions between Roman citizens and foreigners. This made trade much more fluid and allowed the Empire to maintain stable trade relations with other civilizations such as the Phoenicians, Greeks, or the peoples of Asia Minor. 🌍💼

A very important aspect that these laws regulated was the rent of land. During the Empire, many lands belonged to the State, but were leased to wealthy citizens. These lands were mainly used for agriculture and were key to feeding the huge population of the Empire. If a landowner did not pay the rent or did not respect the conditions of the contract, the laws allowed the State to recover those lands. 👨🌾👩🌾

In addition, with the growth of maritime trade, the Romans created specific laws for charter contracts, which regulated how merchandise was carried on ships and what happened if there was an accident or theft during the journey. So if you were a merchant shipping wine from Gaul to Alexandria, you didn't have to worry too much: Roman laws had your back! 🍷⛴️

3. The circulation of coins throughout the empire: The power of the denarius! 💵🌍

Now we are going to talk about something crucial to the Roman economy: currency. One of the greatest achievements of the Empire was monetary uniformity, which facilitated trade and the exchange of goods throughout its vast territories. Before the Romans, each region had its own monetary system, which complicated trade and administration. However, under the reign of Augustus (27 BC – 14 AD), Rome standardized the use of the denarius, a silver coin that became the most common means of exchange throughout the Empire. 🪙

The denarius was the most widely used coin during the Early Roman Empire and circulated widely in places as far away as Britain, Egypt, Hispania, and Asia Minor. This centralized control of the monetary system allowed the Roman Empire to have an integrated economy, where merchants did not have to deal with complicated exchange rates when moving goods between provinces. 📊🌍

But... how did it work? 🧐

The Romans had a hierarchical structure of coins. Aside from the silver denarius, there were other coins such as the sestertius (made of bronze) and the aureus (made of gold). The denarius was the most common and was worth 4 sesterces. This system allowed both the rich and the poor to make transactions. A kind of "economy for everyone"! 😄

The denarius not only facilitated trade within the Empire, but also helped finance Rome's wars and territorial expansion. For example, during Julius Caesar's campaigns in Gaul (58-50 BC), war spoils in the form of precious metals were brought to Rome, where millions of denarii were minted. This allowed trade to grow, soldiers to receive their pay, and state coffers to fill. 🏛️⚔️

An interesting example of the use of currency throughout the Empire was the Silk Road, which connected Rome to China through intermediary traders. Roman denarii were even found in archaeological excavations in places as far away as India and China, proving that the Romans were part of a global trade network. Amazing, right?! 🌏💰

Another important aspect is that the Romans often minted coins with the image of the emperor, which gave them a propaganda function. Yes! Not only were they useful for paying for goods and services, but they also reminded everyone who was in power. You could see the face of Augustus, Nero, or Trajan on every coin, ensuring that their image traveled throughout the Empire, from the borders of Germania to the markets of Alexandria. 🪙👑

Epilogue: Rome, the economic pioneer of the ancient world 📈🏛️

The Roman Empire was much more than invincible legions and gladiators in the Colosseum. Its economic success was one of the pillars that allowed it to sustain itself for centuries. From the argentarii who offered loans in the markets of Rome, to the laws that regulated trade throughout the Mediterranean, to the standardization of the denarius, Rome created an economic system that integrated millions of people into a single monetary and legal framework.

In short, the Romans pioneered many of the economic ideas that we take for granted today. They were the first to develop a primitive banking system, create laws protecting property and regulating trade, and establish a currency that circulated throughout their vast empire. Their legacy lives on today in many aspects of our modern economy. 😎💡

🏰The Middle Ages:

laid the foundations of finance

Welcome to the fascinating world of the Middle Ages! 🛡⛪ This period, spanning from the fall of the Western Roman Empire in 476 AD to the beginning of the Renaissance in the 15th century, is filled with economic, social and political transformations that shaped the history of Europe. Get ready for a medieval history lesson like you've never seen before! 🏰📜💸

1. Feudalism: The “I protect you, you farm me"🏰🌾

Let’s start with the basics. What is feudalism? Feudalism was the predominant economic and social structure throughout most of the Middle Ages, especially in Western Europe.

It was born in response to the collapse of the Roman Empire, where there was no longer a strong central government to maintain security and order. Without the protection of a powerful state, people began to group around feudal lords, who were basically local chieftains who promised military protection in exchange for labor and agricultural products. It’s a bit like saying, “you farm my land, and I’ll protect you from Viking raids.” 🛡️⚔️

In this system, the feudal lord owned large tracts of land, known as fiefs, and peasants (or serfs) worked those lands. Serfs were not technically slaves, but they were not free either: they were tied to the land, meaning that if someone sold the fief, the serf "came included" in the package. The economy at this time was mostly agricultural, and production was based on self-sufficiency: what was produced on the fief was consumed there. 🍞🌾

But not everything was about working the land and protecting oneself from barbarian invaders. Medieval castles became the center of economic and social activity. Small markets arose around them where peasants could sell their surplus production and buy tools or products that they could not produce themselves, such as iron utensils or woolen clothing.

In short, feudalism was like an exchange:

the lord protected you and gave you land to work, and in exchange, you paid him with work and a part of your harvest. An economy based on security and land, where trade did not yet have the same weight that it would later gain. 🏞️🌻

2. The rise of guilds: The control of medieval trade! ⚒️🏙️

While feudalism was taking its course in the countryside, something very interesting was happening in the cities: the guilds. 🌆 These were associations of artisans and merchants that emerged in the High Middle Ages (from the 11th century onwards) to regulate and control commercial activities in each city or region. Imagine that you are a medieval shoemaker in Paris, and you want to sell your products; in order to do so, you had to belong to the shoemakers' guild. 🎒👞

Guilds were not just trade associations, they also had a very important social function. They controlled the quality of products, regulated prices, and even decided who could open a business in the city. This created a kind of local monopoly, as only guild members could sell products in a city. This had its good side, as it guaranteed that the products were of good quality and that the artisans lived with dignity, but it also greatly limited competition. 😲

One of the most powerful guilds of the Middle Ages was the weavers' guild in cities such as Florence and Bruges, where the production of cloth was one of the pillars of the local economy. These cities became authentic industrial centers, where wool and silk were produced in large quantities and then distributed throughout Europe. 🧶🌍

In addition to artisans, merchants also formed guilds to protect their interests. For example, merchants engaged in long-distance trade, such as those carrying wine from France to England, or spices from the East to Venice, also formed associations to defend themselves against abusive taxes or thieves who might attack their caravans. 🚚🍇

3. Early forms of bills of exchange and credit: The medieval innovation of virtual money! 💵✉️

One of the great economic advances of the Middle Ages was the emergence of bills of exchange and credit. At a time when traveling long distances was dangerous and carrying large sums of cash could be a recipe for disaster (bandits were a constant threat! 🏴☠️), merchants began using a kind of "promissory notes" or bills of exchange to move money without needing to physically carry it.

The bill of exchange was a document that allowed a merchant to transfer payment through another merchant in a different city. For example, a merchant in Genoa who wanted to buy wool in Flanders could issue a bill of exchange that would be paid by a banker in Flanders, rather than carrying a bag of coins halfway across the continent. Imagine that! It was like having a medieval credit card. 💳🏦

This system allowed for the growth of international trade in the Late Middle Ages (13th century onwards) and was one of the foundations for the creation of the modern financial system. In addition, this method helped to avoid taxes and exchange rates, which were often different in each region. Merchants became experts in using these tools, and soon bills of exchange were accepted by bankers in cities such as Venice, Florence, and Barcelona.

4. Creation of the first banking houses in Italy: The financial pioneers 💼💶

Italy, during the Middle Ages, was the economic heart of Europe, and it was there that the first modern banking houses emerged. 🌍💰 During the 13th and 14th centuries, Italian city-states such as Florence, Venice, and Genoa became true centers of trade and finance, with powerful families controlling much of the economy.

The term "banking" comes from the Italian word "banco," which refers to the tables where bankers conducted their transactions in the markets. Italian bankers were known for their skill in managing credit, issuing loans, and creating complex accounting systems. 😎

One of the earliest and most famous banking houses was that of the Medici, an influential banking family in Florence. The Medici not only grew rich by controlling trade and lending, but also became great patrons of art and culture, funding artists such as Michelangelo and Leonardo da Vinci. 🖼️🎨 But it wasn't just the Medici; families like the Bardi or the Peruzzi also dominated finance and lent money to kings, popes and merchants across Europe.

These banking houses were the first to implement double-entry accounting systems, which allowed them to keep a more accurate record of their transactions. In addition, they developed international networks of agents, which facilitated the circulation of money and credit across the continent. These Italian bankers laid the groundwork for what would later become modern capitalism. 💶🌐

5. Control of trade in Europe: Routes and fairs 🛍️🛣️

During the Middle Ages, trade was not limited to small local markets or transactions within fiefdoms. As cities grew and international trade expanded, trade routes emerged connecting Europe to other parts of the world. From the North Sea to the Mediterranean, merchants carried goods from one place to another, creating an interconnected economic network.

In Europe, large trade fairs were key events. One of the most famous was the Champagne Fair in northeastern France, which in the 12th and 13th centuries became the epicenter of European trade. There, merchants from all over Europe gathered to exchange goods such as fabrics, spices, precious metals, and wine. 🍷🧂

And there you have it! 🎉 The medieval economy was far more complex and advanced than we might imagine. From feudalism and guilds, to the financial innovations of Italy, this period laid the groundwork for the economic development of Europe and ultimately the modern world.

🎻Renaissance Economics:

The Pioneers of Credit💲

Welcome to the Renaissance! 🌍🎨 A fascinating period of history that goes beyond the arts and humanism; it was also a key moment in the economic evolution of Europe. During the 14th to 17th centuries, a true economic revolution took place that laid the foundations for modern capitalism. Supply and demand, fundamental concepts that dominate markets today, began to play a crucial role in the economy of this period. In this article, I will take you on a journey through the main economic transformations of the Renaissance, from the rise of trade, banking innovations, to the growth of cities and the influence of key figures. All in a light and easy-to-understand tone. Let's go! 💰📚

1. The Renaissance: More than art and culture, an economic explosion! 🎭💰

Before we dive into the economic details, let's do a quick recap. The Renaissance, which began in Italy in the 14th century and spread throughout Europe in the 15th and 16th centuries, was not only a cultural and artistic movement (although Leonardo da Vinci, Michelangelo, and other art giants were born there). It was also a time of economic transformation driven by the rediscovery of classical texts, the expansion of trade, and a growing demand for goods and services. 🌍📈

The Middle Ages had left behind a feudal system based largely on agriculture and local control of resources, but in the Renaissance, this began to change. Europe experienced a process of urbanization, the growth of trade, and the opening of new trade routes to the New World (thanks to navigators such as Christopher Columbus in 1492). All of this contributed to a much more dynamic economy, where the concepts of supply and demand began to take shape more explicitly. 📦🚢

2. The rise of trade and new routes: Supply and demand in motion 🚢⚖️

One of the biggest economic changes of the Renaissance was the rise of international trade. Europe no longer relied exclusively on local agricultural production; cities began to specialize in artisanal production, and merchants became key players in the economy.

Florence and the Medici bankers 💶🏛️

One of the most iconic cities of the Renaissance was Florence. It was not only the center of art and culture, but also of the economy. The Medici family, famous for being patrons of artists such as Leonardo and Michelangelo, was also crucial to the development of banking in Europe. The Medici controlled one of the most powerful banking houses in Europe, which financed kings, popes, and merchants.

But it was not only Florence that played a role in economic growth. Italian city-states such as Venice and Genoa became commercial centers thanks to their strategic location on the Mediterranean Sea. These cities prospered by trading luxury goods such as spices, silk, and gold from the Far East and the New World. 🧂🌶️

This international trade brought with it a real explosion of supply and demand. The demand for exotic products in Europe increased, causing merchants and businessmen to compete to bring in more and better products. For example, silk and spices were so valuable that they were sold at astronomical prices. This in turn spurred the offering of new trade routes, such as the famous Spice Route, which connected Europe to Asia across the Indian Ocean. A real money-making business! 💼🌍

Spain and Portugal: The Giants of the New World ⚓🗺️

With the arrival of explorers such as Christopher Columbus (who reached America in 1492) and Vasco da Gama (who reached India in 1498), new trade routes were opened that connected Europe to the Americas, Africa and Asia. These discoveries brought with them a flood of new goods, such as gold and silver from America, as well as agricultural products such as cocoa, potatoes and tobacco. This radically changed the European economy.

Demand for these new products in Europe increased exponentially, while supply was limited by the difficulty of extracting and transporting these goods across the Atlantic. Of course, demand outstripped supply in many cases, driving up the price of products like cocoa and tobacco. European merchants grew rich, and port cities like Seville and Lisbon flourished. ⚓💰

The Hanseatic League: Trade in Northern Europe ⛵🏴

While Southern Europe prospered from Mediterranean trade, Northern Europe was not far behind. The Hanseatic League, an alliance of trading cities on the Baltic and North Seas (such as Hamburg, Lübeck, and Bremen), controlled much of the trade in goods such as grain, timber, and metals. Although the League had begun in the Middle Ages, it was during the Renaissance that it reached its peak.

Here, supply and demand also dictated

the pace of trade. Northern cities relied on grain

and agricultural products from Eastern Europe,

while exporting manufactured goods to other

parts of the continent. This system continued for centuries, and the Hanseatic League was instrumental in creating a trade network that connected Europe from the Baltic countries to the Netherlands. 🌾🛳️

3. Banking and Financial Innovations: The Pioneers of Credit 💳🏦

The Renaissance saw the birth of many of the financial systems we still use today. International trade required more sophisticated methods of handling money, and Renaissance bankers rose to the challenge. It was here that the concepts of credit, interest, and bills of exchange (as we saw them in the Middle Ages) were refined and spread throughout Europe.

Florentine banking and the Medici 🏛️💰

If there is one family that marked financial development in Europe during the Renaissance, it is the Medici family. The Medici were not only patrons of art, they were also pioneers of the modern banking system. Under their leadership, Florence became the financial center of Europe. Their bank operated in many major European cities, offering loans and facilitating international trade.

One of the great innovations of Renaissance bankers was the use of bills of exchange and long-term loans, which allowed merchants and nobles to make large investments without needing to carry huge sums of cash with them (much safer!). They also began to charge interest, something that was previously frowned upon by the Church, but which was slowly accepted as part of the business. 📜💶

The first banking houses in Europe 🏦💶

In addition to the Medici, many other Italian cities were pioneers in the development of banking. In Venice, for example, some of the first public financial institutions emerged, such as the Bank of San Giorgio, founded in 1407 in Genoa. This bank was one of the first to offer credit and handle deposits, laying the foundations for the modern financial system. This system not only helped merchants, but also local governments, which turned to bankers to finance their projects (and their wars, of course).

The supply and demand for credit grew, leading to the creation of new financial institutions in cities such as London and Antwerp. Bankers became key figures in the economy, as they could finance large commercial ventures and expeditions to far-off places. 🚢💳

4. The explosion of urban trade: Cities, markets, and the rise of supply and demand 🏙️🛍️

One of the most interesting aspects of the Renaissance was the growth of cities and their transformation into centers of trade and production. In cities such as Florence, Venice, Antwerp, Amsterdam, and London, local markets and trade fairs attracted merchants from around the world.

Antwerp: The Wall Street of the Renaissance 📈🏛️

During the 16th century, the city of Antwerp (in present-day Belgium) became Europe's main trading centre. This is where some of the world's most important commercial transactions took place. Its port, strategically located on the Scheldt River, allowed access to goods from America, Asia and Africa.

In Antwerp, the supply of exotic products from around the world met European demand. The result was a vibrant and ever-expanding market. The city was home to the first stock exchange (established in 1531), where goods, stocks and government debt were traded. Antwerp was the financial epicentre of Europe for much of the 16th century. 🏦💸

Conclusion: The Renaissance and the economics of supply and demand ⚖️🌍

The Renaissance was a period of profound economic transformation. The expansion of international trade, the rise of cities, and financial innovation allowed the concepts of supply and demand to become determining forces in the European economy. Renaissance bankers, merchants, and traders laid the groundwork for many of the economic practices we still use today.

The Industrial Revolution: A Brief Analysis of the Economy and Finance of the Time 🚂💰

Greetings, history buffs! Today we're going to explore a fascinating topic: the Industrial Revolution and its impact on the economy, supply and demand, as well as the key figures and financial changes that shaped the modern world. Get ready for a journey full of information and excitement! 🎉

Historical Context: What was the Industrial Revolution? 🤔

The Industrial Revolution was a period of radical transformation that began in Britain in the late 18th century and lasted until the mid-19th century. This process involved the shift from an agrarian, artisanal economy to an industrialized, mechanized economy. From the invention of the steam engine to the development of massive factories, it was all a huge step forward. 🌍

The Economy in Transformation 💹

The economy during the Industrial Revolution underwent a number of significant changes that altered the way people produced, consumed, and distributed goods.

Mass Production: The introduction of machinery revolutionized production. Factories began to operate on a large scale, producing goods such as cloth, steel, and machinery. Before, a weaver could make just a few pieces a day; now, with the spinning machine, they could produce thousands. This led to a dramatic increase in the supply of goods. 🏭

Law of Supply and Demand: With mass production, supply outstripped demand in some cases, leading to a reduction in prices. However, as more people had access to products once considered luxuries, demand increased again. This continuous cycle of supply and demand became a fundamental principle of modern economics. 📉📈

Emerging Markets: The Industrial Revolution also fostered the creation of new markets. With increased production and consumption, more complex trade networks were established, and new products emerged that created niche markets. This was especially evident in the textile industry, where demand for cotton increased greatly. 👗

Key Figures: The Innovators of the Age 🦸♂️

The Industrial Revolution was not just a technological movement; it was driven by visionary individuals who set the tone.

James Watt:

His improvement of the steam engine in 1769 not only increased efficiency in factories, but also allowed its use in locomotives and ships, revolutionizing transportation. This facilitated trade and the distribution of products. 🚂

Richard Arkwright:

With his spinning machine, also known as the "Spinning Frame", he laid the groundwork for mass production in the textile industry. Arkwright is considered one of the first to implement modern manufacturing in its purest form. 👕

Adam Smith:

Although his work "The Wealth of Nations" was published in 1776, his ideas on the market economy and the "invisible hand" describe how competition drives innovation and efficiency. His influence was felt throughout the Industrial Revolution and still endures today. 📚

Financing and Capitalization: Money at Play 🏦

Financing became a crucial element for industrial development. As factories needed capital to buy machinery and hire workers, the financial system also evolved.

Banks and Loans: Banks began to play a vital role, offering loans to entrepreneurs who wanted to invest in new technologies. This created broader access to capital, facilitating business growth.

Shares and the Stock Market: The creation of the London Stock Exchange in 1801 allowed investors to buy shares in companies, diversifying their investments and providing essential capital to new businesses. This financing system was critical to the growth of industry. 📈

Investment in Infrastructure: Railways, one of the most significant achievements of the Industrial Revolution, required massive investment. Private capital, along with government support, helped build rail networks that connected cities and regions, further boosting the economy. 🚄

Social Impact: Changes in the Structure of Society 👥

The Industrial Revolution not only transformed the economy; it also had a profound impact on society.

Urbanization: As people migrated from the countryside to the cities in search of work, new urban areas emerged. Cities grew rapidly, creating new challenges such as overpopulation and lack of public services. 🌆

Working Conditions: Despite the creation of jobs, working conditions were often inhumane. 12- to 16-hour work days, low wages, and a dangerous work environment were common. This led to labor movements and eventual labor reform in the years that followed. ⚖️

Emerging Social Classes: The Industrial Revolution saw the rise of a new middle class, made up of entrepreneurs and industrialists. At the same time, the working class was also consolidated, which would begin to demand rights and better conditions. This change in social structure would be crucial for future political development. 🏙️

Conclusions: A Lasting Legacy 🌟